VAT Margin Scheme & Global Accounting Scheme (Margin Scheme)

VAT can often create cash flow pressure for businesses dealing in second-hand goods, antiques, collectibles, or low-margin resale stock. The VAT Margin Scheme and its simplified variant, the Global Accounting Scheme (also known as global margin accounting), are designed to ensure businesses only pay VAT on their actual profit margin rather than the full selling price.

For VAT-registered traders, particularly dealers in second-hand goods, these schemes can significantly improve competitiveness and cash flow efficiency when applied correctly and with robust compliance procedures.

What is the VAT Margin Scheme?

The VAT Margin Scheme is a special VAT accounting method that allows eligible businesses to account for VAT on the difference between the purchase price and selling price, rather than on the full selling price of goods.

In simple terms:

VAT is charged only on the profit margin

The standard VAT fraction of 1/6 (16.67%) is applied to the margin

The scheme is designed to avoid double taxation where goods have already been subject to VAT in a previous supply chain

This is particularly relevant for goods acquired from private individuals or non-VAT registered suppliers where no input VAT has been reclaimed.

Example:

Purchase price: £1,000

Selling price: £1,500

Margin: £500

VAT due: £83.33 (1/6 of £500)

This approach ensures VAT is only applied to the value added by the business, not the full resale value.

Which Goods Qualify for the Margin Scheme?

The VAT Margin Scheme is typically available for:

Second-hand goods

Antiques

Works of art

Collectors’ items

However, strict exclusions apply. The scheme cannot be used where:

VAT was charged on the original purchase invoice

Goods are investment gold or precious metals

Certain imported goods fall outside qualifying conditions

Businesses must carefully assess stock eligibility at the point of acquisition, as incorrect classification can lead to VAT assessments and penalties.

Global Accounting Scheme (Simplified Margin Scheme)

For businesses trading in high-volume, low-value second-hand goods, HMRC provides a simplified alternative known as the Global Accounting Scheme.

Rather than calculating VAT item-by-item, businesses calculate VAT based on the overall margin for the VAT period:

Total sales of eligible goods

minus Total purchases of eligible goods

= Net margin subject to VAT

VAT is then applied at 1/6 of the global margin.

📌 This scheme is particularly useful where:

Individual stock records are impractical

Businesses handle large volumes of low-value goods

Stock is frequently rotated or bundled

Administrative burden under the standard margin scheme is too high

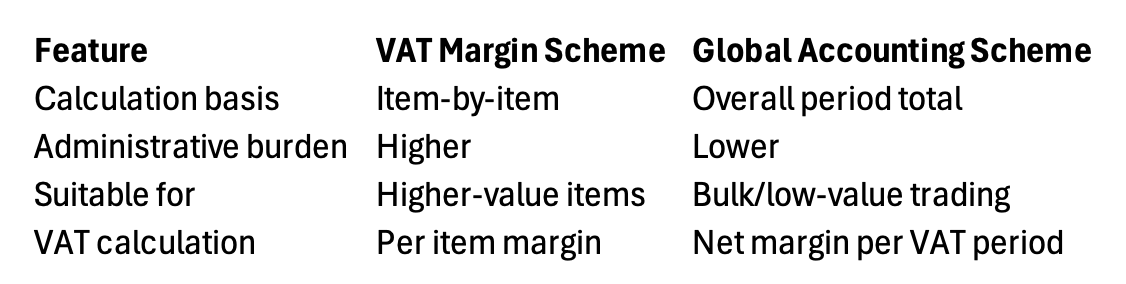

Key Differences: Margin Scheme vs Global Accounting Scheme

How VAT is Calculated Under Both Schemes

Under both systems:

VAT is charged at 1/6 of the margin

Loss-making items do not generate VAT liability

Negative margins can be carried forward (under global accounting rules)

Importantly, VAT is not recoverable on purchases within the scheme, but VAT on overheads (e.g. professional fees, rent, software) remains recoverable under normal VAT rules.

Record Keeping and Compliance Requirements

HMRC places strict emphasis on documentation. Businesses must maintain:

Purchase and sales records for each eligible item (or aggregated records under global accounting)

Evidence of purchase price and supplier details

Clear identification of eligible and non-eligible stock

Failure to maintain adequate records may result in VAT being due on the full selling price rather than the margin.

Common Compliance Risks

Applying the scheme to ineligible goods

Mixing standard VAT accounting with margin scheme stock incorrectly

Missing or incomplete purchase documentation

Incorrect treatment of imported second-hand goods

Applying VAT on selling price instead of margin

These issues are frequently identified during HMRC VAT inspections in resale businesses.

Strategic VAT Planning Considerations

For many retail and resale businesses, the margin schemes can provide:

Improved cash flow (VAT delayed and reduced)

Lower effective VAT liability

More competitive pricing flexibility

Simplified accounting (especially under global accounting)

However, scheme selection should always be based on:

Business model and stock type

Average transaction value

Record-keeping capacity

VAT registration status and turnover profile

Final Thoughts

The VAT Margin Scheme and Global Accounting Scheme are powerful VAT simplification tools when used correctly. However, they are also highly technical, and incorrect application can result in significant VAT assessments.

Professional advice is strongly recommended before adopting or transitioning between schemes, particularly where businesses deal in mixed stock types or cross-border supply chains.

At Surrey Hills Tax, we advise businesses on VAT structuring, margin scheme compliance, and HMRC enquiries to ensure full compliance while optimising tax efficiency.

Disclaimer: This article is for general information only and does not constitute tax advice. Tax treatment depends on individual circumstances and may change.